Edge

Edge Chrome

Chrome Firefox

Firefox

转载一段 seekalpha 上的分析. 作者 Stuart Allsopp

原文: https://seekingalpha.com/article/4652574-qqq-3-reasons-sell-rate-cut-euphoria

文章发表时间是 11月17日, 文章整体观点偏空

---------------

即使美联储如预期积极宽松,昂贵的估值、增长放缓和普遍的乐观情绪也将成为收益的阻力

主要风险来自对恰到好处的的宏观情景,即通胀下降和增长复苏的期盼,但目前前瞻的指标表明这不太可能

High Yield Corporate Credit Spreads Vs Interest Rates (Bloomberg)

NDX PE Ratio Vs Fed Funds (Bloomberg)

NDX Vs SPX Small Cap PE Ratios (Bloomberg)

The Market Ear, MS QDS

(正文完)

----------------------------------

再摘抄一些评论

评论1:

评论2:

评论3:

监管机构似乎不像过去那样拆分准垄断企业,因此大型科技公司不断吞并有前途的初创公司。许多规模较小、大致相等的竞争对手意味着低利润,少数大型参与者意味着高利润。这就是纳指7雄如此强势的原因。

评论4:

原文: https://seekingalpha.com/article/4652574-qqq-3-reasons-sell-rate-cut-euphoria

文章发表时间是 11月17日, 文章整体观点偏空

---------------

Summary

- The QQQ has ripped higher amid renewed expectations of interest rate cuts in 2024, but history shows that rate cuts tend to only occur after market declines.

- Even if the Fed eases aggressively as expected, expensive valuations, slowing growth, and widespread bullishness will act as headwinds to gains.

- The main risk comes from a Goldilocks macro scenario where inflation falls and growth recovers, but leading indicators suggest this is unlikely.

概要:

由于对2024年降息的预期再次出现,QQQ大幅走高,但历史表明,降息往往只发生在市场下跌之后即使美联储如预期积极宽松,昂贵的估值、增长放缓和普遍的乐观情绪也将成为收益的阻力

主要风险来自对恰到好处的的宏观情景,即通胀下降和增长复苏的期盼,但目前前瞻的指标表明这不太可能

A lot has changed since my last update on the benchmark Nasdaq 100 ETF, Invesco QQQ Trust (NASDAQ:QQQ) in early September. The ETF, which is the largest and most liquid ETF tracking the Nasdaq 100, dropped 10% to its October lows amid fears of higher for longer interest rates, before weakening macro and inflation data triggered a major three-week rally, bringing the QQQ back to its July 7 highs. Bulls are looking for a repeat of 2019 when a mild economic slowdown allowed monetary easing to drive the QQQ higher. However, I see three reasons why this is unlikely.自9月初我上次更新纳斯达克100指数ETF(股票代码:QQQ)以来,情况发生了很大变化。由于担心长期利率会上升,该ETF下跌了10%至10月低点,随后宏观和通胀数据疲软引发了为期三周的大幅反弹,使QQQ回到7月7日的高点。2019年牛市似乎正在重演,当时温和的经济放缓允许货币宽松推动QQQ走高。然而,我认为这不太可能, 原因有以下三个:

1: Rate Cuts Will Likely Require Equity Market Weakness

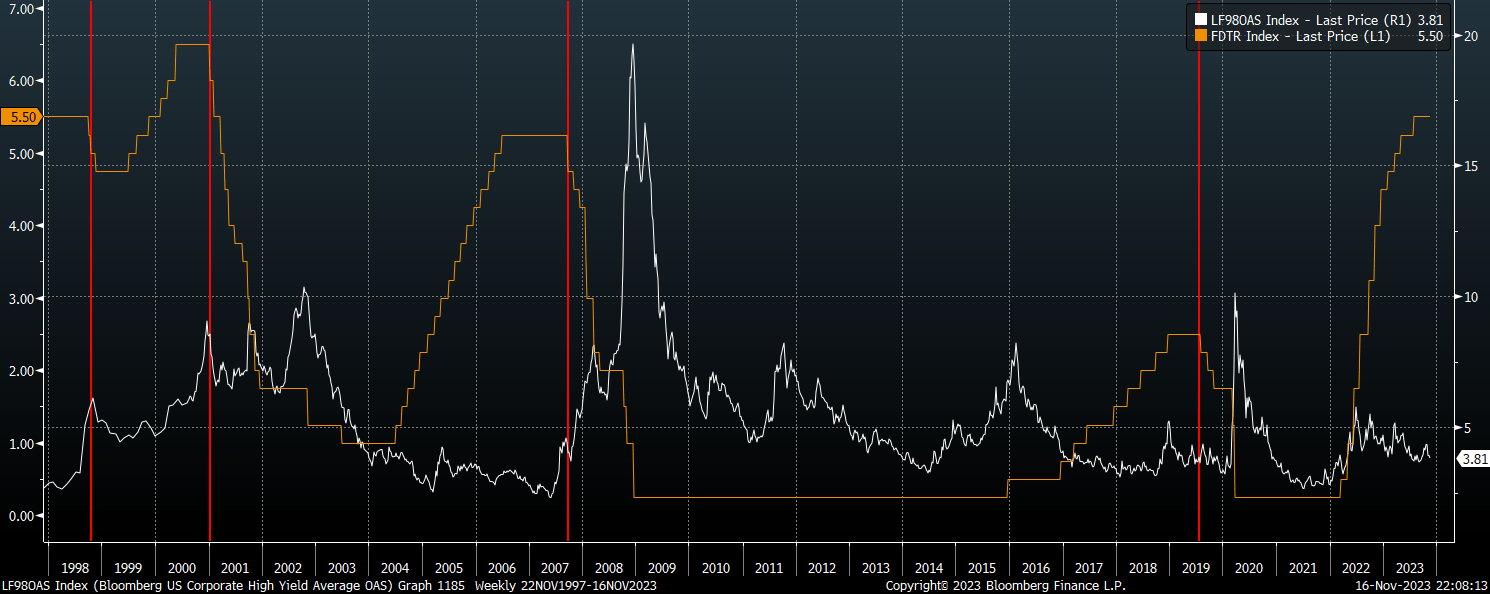

The slight miss in US October CPI has increased expectations of rate cuts in 2024, with markets now pricing in 100bps of cuts between now and December next year. I have no particular view on that, but the problem for the QQQ is that over the past 25 years, the Fed has never cut rates until after a spike in credit stress, which has tended to also undermine stocks. This can be seen in the chart below which shows US high-yield credit spreads against the Fed funds rate.

降息可能需要股市先表现疲软

美国10月CPI的小幅下跌增加了投资者对2024年降息的预期,市场目前预计从现在到明年12月将降息100个基点。我对此并没有特别的看法,但QQQ的问题是,在过去25年里,美联储在信贷压力飙升之前从未主动降息,而信贷压力飙升也往往会破坏股市。这可以从下图中看出,该图显示了美国高收益信贷相对于美联储基金利率的利差。

High Yield Corporate Credit Spreads Vs Interest Rates (Bloomberg)

Even the slight easing that occurred in H2 2019 was preceded 8 months earlier by a 230bps spike in credit spreads and a 20% fall in the QQQ, and CPI was running below 2% at the time. This is the reason why rate cuts are often bullish for stocks, as they happen only after stocks have already declined and are often cheap and oversold. This is not the case today.即使是2019年下半年出现的小幅宽松,也是在8个月前出现了230个基点的信贷利差飙升后的现象,这段时间内 QQQ 经历了 20%的下跌,当时CPI低于2%。这就是为什么降息通常对股票有利的原因,因为只有在股票已经下跌且往往价格低廉且超卖之后才会降息。然而今天的情况并非如此。

2: Valuations Are More Expensive And The Growth Outlook Weaker

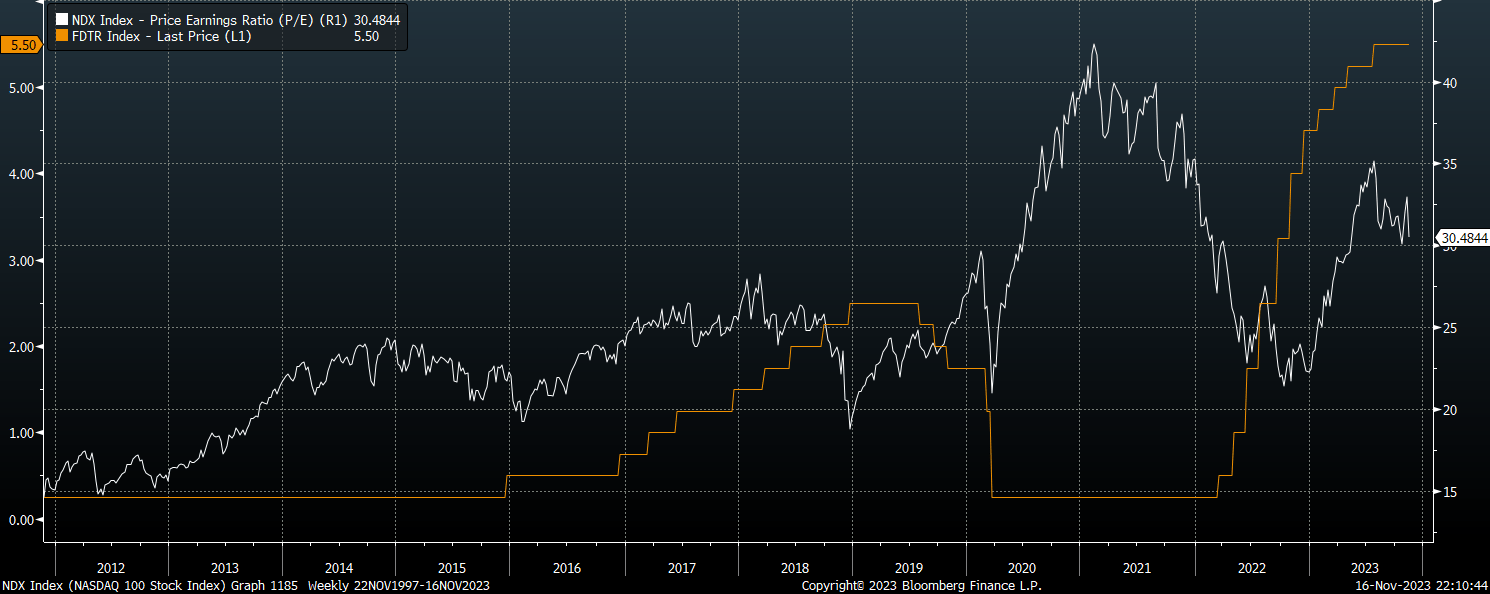

This brings me to the second point which is that the H2 2019 rally that followed the beginning of monetary easing began when the PE ratio on the QQQ was around 23x compared to over 30x today. Furthermore, total Nasdaq 100 earnings were 27% of the S&P 500 back then compared to 35% now.

估值更贵,并且增长前景疲软

货币宽松开始后的2019年下半年反弹始于QQQ的市盈率约为23倍,而今天超过了30倍。此外,纳斯达克100指数当时的总收益为标准普尔500指数的27%,而现在为35%。

NDX PE Ratio Vs Fed Funds (Bloomberg)

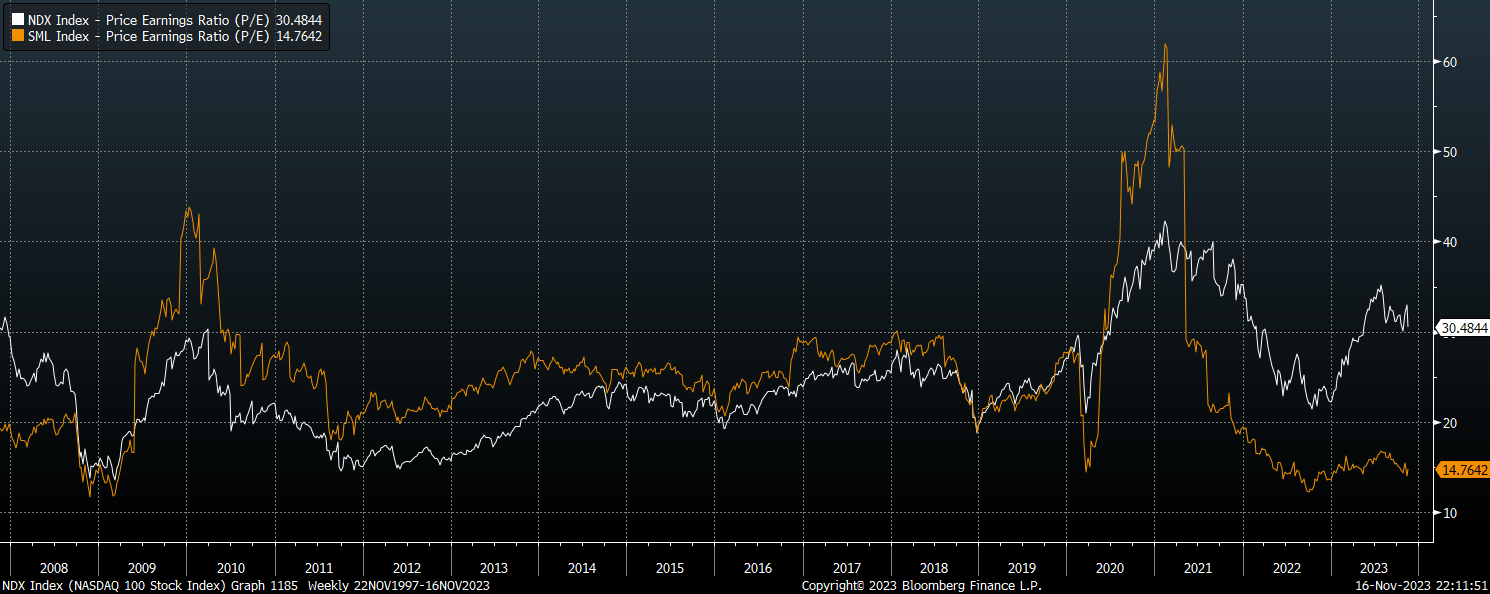

For the longest time, US investors have applied a discount to the largest stocks in the market. For almost a full decade prior to COVID-19, the median S&P 500 stock traded at a higher PE ratio than the overall index. Furthermore, the NDX traded at a large discount to small-cap stocks throughout this period.在很长的一段时间里,美国投资者对市场上大市值股票的股价是需要一定折扣的。在新冠肺炎爆发前的近十年里,标普500指数成份股的市盈率中值高于整体指数。此外,在此期间,纳斯达克指数的交易价格大大低于小盘股。

NDX Vs SPX Small Cap PE Ratios (Bloomberg)

The reason for this discount is that larger companies have tended to experience slower long-term growth, which has outweighed the positive impact of factors such as stable earnings and strong balance sheets. Growth is a function of market penetration and economic growth, and with NDX 100 earnings now at 35% of the whole US market, up from 20% a decade ago, earnings growth should converge to the rate of nominal GDP growth.折价存在的原因是,大型公司往往经历较慢的长期增长,这超过了稳定收益和强劲资产负债表等因素的积极影响。增长是市场渗透率和经济增长的函数,鉴于纳斯达克100收益目前占整个美国市场的35%,高于十年前的20%,收益增长应收敛于名义GDP增长率。

NDX earnings have outpaced nominal GDP growth by around 8% over the past decade, with sales growing 5% faster and rising margins accounting for the rest of the outperformance. If this were to continue for another decade NDX earnings would rise to around 75% of the overall market from 35% currently, assuming SPX earnings keep pace with GDP growth. This is unrealistic and so a slowdown in growth relative to the economy and the S&P 500 is inevitable.在过去十年中,纳斯达克指数的收益超过名义GDP增长约8%,营收增长速度快5%,剩余部分则是利润率的上升。如果这种情况再持续十年,假设标普指数的收益与GDP增长保持同步,纳斯达克指数收益将从目前的35%上升到整体市场的75%左右。这是不现实的,因此相对于经济和标准普尔500指数而言,纳斯达克指数增长放缓是不可避免的

Even if we assume that current near-record margins remain intact and sales growth continues to outperform the economy by 5%, this is likely to result in less than 10% annual returns assuming 4% trend GDP growth, with the dividend yield adding less than 1%. This would put the QQQ near fair value as stocks have typically outperformed bonds by around 5% annually.假设目前的利润率保持不变,营收增长继续优于经济5%,假设GDP增长趋势为4%,而股息收益率增加不到1%,这也可能导致年回报率不到10%。这将使QQQ接近公允价值,因为股票通常每年的表现优于债券约5%。

If NDX earnings growth were to slow to the pace of the overall economy over the next decade as I expect, this would put QQQ returns in line with bonds. This may sound fine, but if investors are anticipating perpetual 5% earnings growth outperformance and 10% total returns, then a major decline in valuations could result. If investors were to implicitly require QQQ to return 10% annually amid 4% earnings growth and a 0.8% dividend yield, this would require an 88% decline in valuations. Such is the sensitivity of expensive stocks to growth assumptions.如果纳斯达克指数的收益增长如我所预期的那样在未来十年放缓到整体经济的速度,那么QQQ的回报率将与债券持平。这听起来可能不错,但如果投资者预期收益增长率将永远超过整体经济 5%,总回报率将达到10%,那么估值可能会大幅下降。如果投资者隐含地要求QQQ在4%的收益增长率和0.8%的股息收益率下每年回报10%,那么这将要求估值下降88%。这就是昂贵股票对增长假设的敏感性。

3: Tech Stocks Are Already Universally Loved

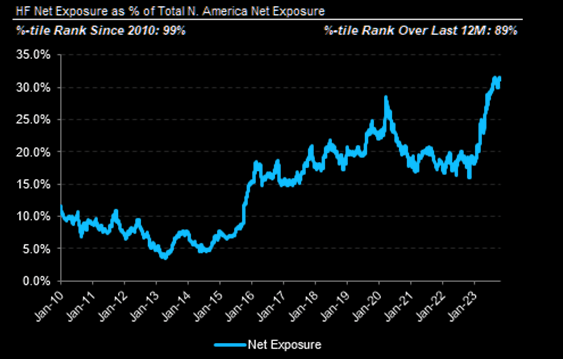

It appears that a melt up in the QQQ would surprise very few investors. Not one Wall Street analyst has a sell recommendation on Google (GOOG) (GOOGL), Amazon (AMZN), Nvidia (NVDA), or Microsoft (MSFT), and the percentage buy rating ranges from 85% in the case of Google to 97% in the case of Amazon. Meanwhile, hedge funds are fully loaded up on Mega Cap tech, with net exposure running in the 99% percentile since 2010.

人人都爱科技股

很少人会惊讶于QQQ的融涨。没有一位华尔街分析师对谷歌(Google)、亚马逊(Amazon)、英伟达(Nvidia)或微软(Microsoft)提出过卖出建议,买入评级的百分比从谷歌的85%到亚马逊的97%不等。与此同时,对冲基金正全力投资大盘股科技,自2010年以来,净敞口已达到99%。

The Market Ear, MS QDS

I remember back in 2013 when hedge fund exposure was below 4% on the chart above. Despite deeply negative real interest rates at the time the forward PE ratio was just 13x, with the dominant narrative that slow growth prospects justified these valuations. The current euphoria surrounding Mega Cap stocks, while not a timing indicator, is cause for caution at the very least.我记得在2013年,对冲基金的风险敞口低于上图中的4%。尽管当时实际利率为负,但远期市盈率仅为13倍,主要的说法是缓慢的增长前景证明了这些估值是正确的。目前围绕大盘股的乐观情绪虽然不是一个时机指标,但至少值得谨慎。

Goldilocks And 1990s Redux Are Two Main Risks我对QQQ持看跌观点的主要风险是,增长和通胀数据继续减弱,足以允许降息,但不足以导致收益预期的大幅下降。然而,领先的经济指标表明,我们还远远没有摆脱2024年上半年经济衰退的困境,而预算赤字很可能会在信贷风险没有任何飙升的情况下使通货膨胀保持高位。

The main risk to my bearish view on the QQQ is that growth and inflation data continue to weaken sufficiently to allow rate cuts but not enough to cause a significant decline in earnings expectations. However, leading economic indicators show we are far from out of the woods regarding a H1 2024 recession, while the budget deficit is likely to keep inflation elevated absent any spike in credit risk.

Another risk is that we see the NDX following the path it took in late-1999 when it turned parabolic from already extremely overvalued levels. However, it is hard to see what kind of narrative could justify such a move as the macro outlook contrasts greatly with that period.另一个风险是,我们看到纳斯达克指数遵循1999年末的路径,当时它从已经被高估的水平变成了抛物线。然而,很难看出什么样的叙述可以证明这样的举措是正确的,因为宏观前景与那段时期形成了巨大对比。

(正文完)

----------------------------------

再摘抄一些评论

评论1:

While QQQ does seem quite overpriced, it might get much more overpriced. I hope you aren't actually short, but own put options instead. If you bought puts, the most you can lose is the cost of the puts.尽管QQQ的价格似乎确实过高,但它可能会被高估得更多。我希望你不是真的做空,而是拥有看跌期权。如果你买入看跌期权,你最多会损失看跌期权的成本。

评论2:

I noticed that you have made 5 Sell calls in as many months. I do not disagree that it is currently expensive; however, isn't it better to buy this high quality index of some of the best companies in the world and then just average on a regular basis into it? I feel that would produce better returns than regularly trying to time the market / guess?我注意到你在几个月内已经5次建议卖出。我不否认QQQ目前很昂贵;然而,购买世界上一些最好公司的高质量指数,然后定期对其进行平均,不是更好吗?我觉得这会产生比定期尝试把握市场/猜测更好的回报.

评论3:

Very sound reasoning, but this was exactly the sort of thought process I went through in approx. 1998 or so: after several years of outperformance and stretched valuations, surely tech stocks had to correct . Well, they did correct eventually, but being right two years early is very much like being wrong.听上去非常合理,但这正是我在大约1998年左右经历的那种思考过程:在几年的表现优异和估值过高之后,科技股一定会回落。嗯,他们最终确实回落了,但提前两年卖出是个错误的决定。

Regulators don’t seem to tear apart quasi monopolies like they used to, so big tech companies keep gobbling up promising upstart startups . Lots of small, roughly equal competitors means low profits (farmers’ eternal plight), few huge players means high profits. Which is why the Mag 7 are so magnificent.

Agreed that rate cuts may only come after something breaks.

监管机构似乎不像过去那样拆分准垄断企业,因此大型科技公司不断吞并有前途的初创公司。许多规模较小、大致相等的竞争对手意味着低利润,少数大型参与者意味着高利润。这就是纳指7雄如此强势的原因。

评论4:

Stick with $QQQ because the top 10 holdings actually make money unlike the top 10 holdings back in 1999. Good luck.坚定持有QQQ,因为目前前十大持股实际上与1999年的前十大持股不同。祝你好运。

京公网安备 11010802031449号

京公网安备 11010802031449号